Understanding Extremal Dependence in Lévy Driven Processes

About

A new study by researchers Zhongwei Zhang, David Bolin, Sebastian Engelke, and Raphaël Huser tackles the open problem of characterizing extreme event dependence in certain non-Gaussian stochastic processes. The work focuses on continuous-time moving average processes driven by exponential-tailed Lévy noise, models that extend classical Gaussian processes to capture heavy deviations and jump discontinuities. Until now, it was unclear how extremes in these models behave jointly across different spatial locations or time points, depending on the domain in which the process is defined.

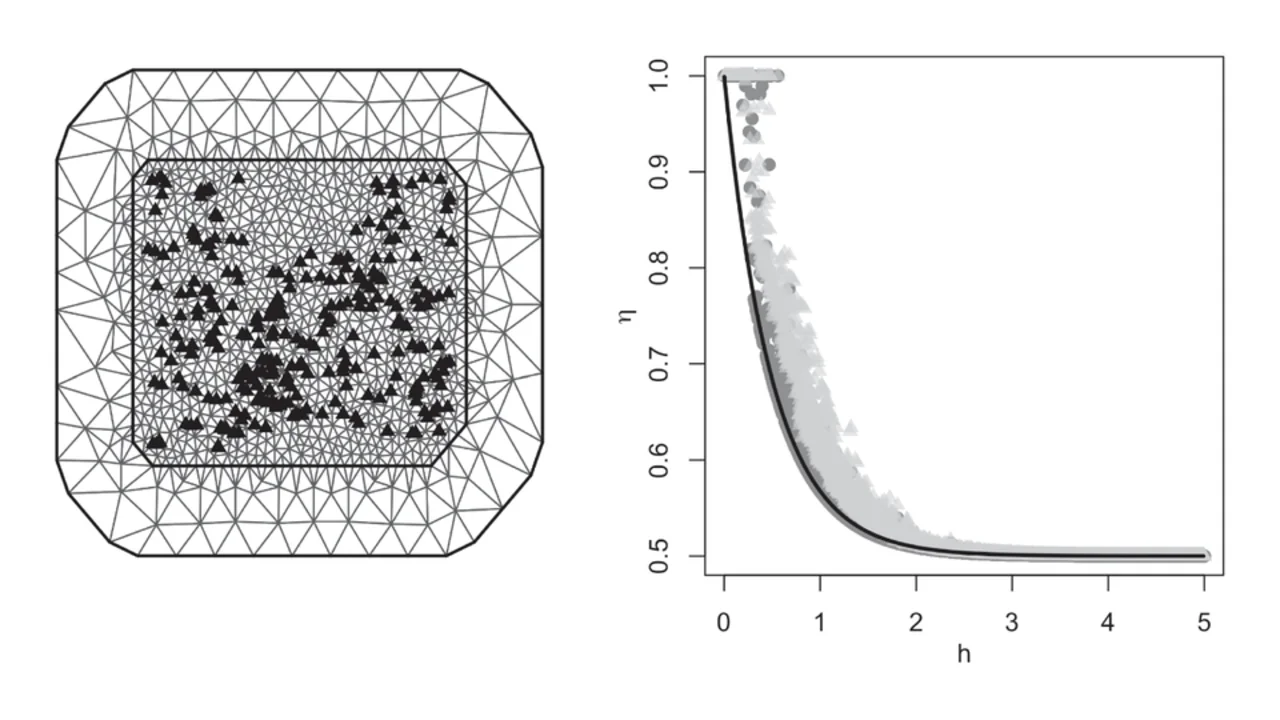

The research develops a framework that connects two regimes of extremal dependence. By leveraging fine grid approximations, the authors demonstrate that these Lévy-driven moving average processes are asymptotically independent when the mesh is sufficiently fine, and provide an explicit expression for the residual tail dependence function in the limiting case. Notably, for the popular Ornstein–Uhlenbeck (OU) process driven by exponential-tailed noise, the study proves it is asymptotically independent as well, albeit with a different tail dependence profile than the Gaussian-case OU process.

These findings provide a flexible and tractable framework for connecting asymptotic dependence and independence in models driven by Lévy noise. The results have important implications for risk modeling in finance, environmental sciences, and other fields where extreme events play a critical role. The study offers new perspectives on how extremes can be represented and analyzed in non-Gaussian models.

REFERENCE:

Zhang, Z., Bolin, D., Engelke, S., & Huser, R. (2025). Tail dependence coefficients of moving average processes driven by exponential-tailed Lévy noise. Extremes, in press.